For warehouse workers, drivers, care workers, retail staff, and laborers who are done being lied to about money.

If you’re working full-time — maybe more — and still going backwards every month, this is for you. Not for people with investment portfolios. Not for people who can “cut back on lattes.” For people who are on their feet all day, driving all day, or caring for others all day, and still can’t seem to get ahead.

The financial advice you see online is mostly useless if you’re earning under $40,000 a year in 2026. Gas is expensive. Rent is brutal. Groceries cost what a full day’s work used to. And the jobs that will “get you out of this” seem to require experience you can’t afford to go get.

You’re not bad with money. The system is genuinely hard right now. But there are real steps — practical ones, not inspirational Instagram quotes — that can stop the bleeding and slowly change your situation. Here they are.

Check out our 6 Month Stability Plan tool for help getting started or head over to money basics.

Free HTF advice

Trying to get your money and career unstuck?

I’m Greg from HTF Finance. I send practical, no-BS advice for working adults who are tired of being told to “just budget better” or “just go back to school” by people who have clearly never had rent, kids, car trouble, and a back that sounds like a haunted staircase.

Join the list for free career path breakdowns, simple money moves, early access to new guides, and first notice when the HTF community opens.

No spam. No lectures. No pretending a side hustle and a spreadsheet can fix a paycheck that is too small.

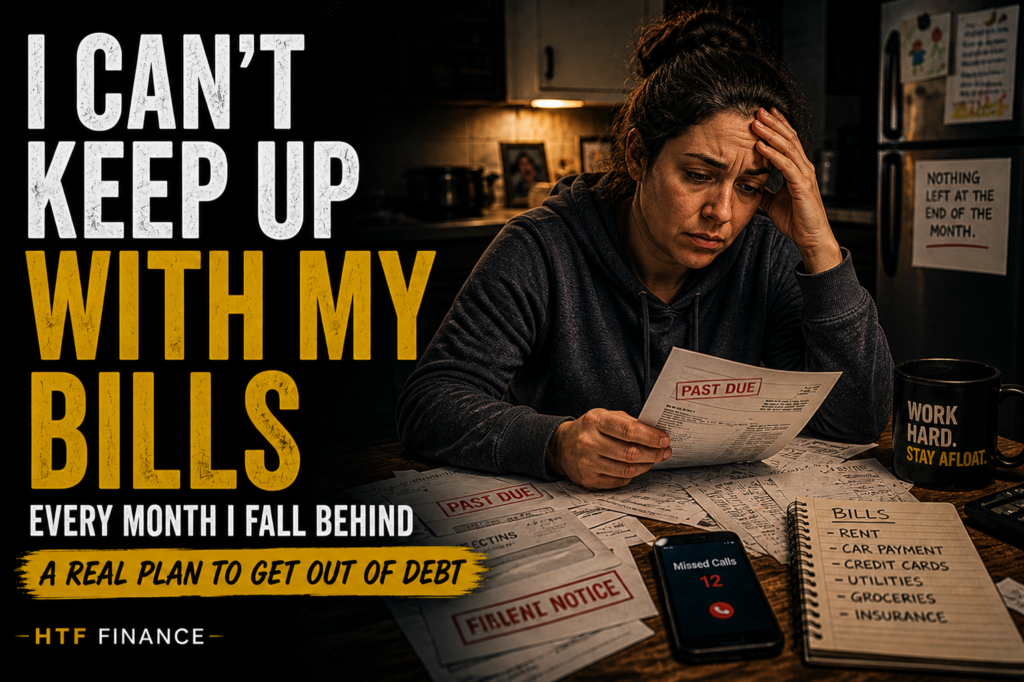

Why Does Debt Feel Impossible to Escape When You’re Working This Hard?

Because the math is rigged against you at low incomes. When you earn $35,000 a year, you take home roughly $2,400 to $2,700 a month depending on your state and situation. Rent, utilities, food, gas, insurance, phone — for most working adults, that’s $2,200 to $2,600 gone before you’ve made a single debt payment. There’s no fat to trim. The problem isn’t habits. It’s that your income doesn’t have enough margin.

Understanding this matters because debt management advice that assumes you have $300 a month spare is useless to you. The steps below work with what you actually have.

Step 1: Know Exactly What You Owe (Even If It’s Scary)

Write down every single debt: who you owe, the balance, the interest rate, and the minimum monthly payment. Medical bills, credit cards, payday loans, car loan, anything. Don’t estimate — pull the actual statements or log into the accounts. Most people avoid this because the number feels overwhelming. But you cannot navigate without knowing where you are.

The total number will probably make you feel sick. That’s okay. You’re not looking at it to feel worse — you’re looking at it so you can actually do something about it.

What Should I Pay Off First When I Can Barely Cover Minimums?

Pay the minimum on everything to stay current. Then take any extra money — even $20, even $10 — and put it all on one debt. Which one? Two approaches work:

The avalanche method: attack the highest interest rate first (usually payday loans or store credit cards). This saves the most money over time.

The snowball method: attack the smallest balance first regardless of rate. This gives you a win faster and many people stick to it better.

When you’re exhausted from work and life is already hard, the snowball method often wins because motivation matters. Pick the one you’ll actually do.

Payday loans first, always. If you have a payday loan, it is your financial emergency. Interest rates of 300% to 400% APR are common. Everything else can wait. Pay that off before anything.

Work with HTF

Need a real plan with step-by-step guidance?

If you’re trying to change careers, fix your money, or both at the same time, you probably don’t need another lecture about discipline. You need someone to help you look at the actual numbers, the actual job options, and the next step that won’t make your life harder.

That’s what Hit The Fan coaching is for. Work with Greg on the 6-Month Stability Plan, one-on-one coaching, or a realistic no-degree career path that fits your actual life.

No lectures. Just the next better step.

Is There Anything I Can Do to Lower the Interest I’m Paying?

Call your creditors and ask for a lower rate. This sounds too simple, but it works surprisingly often — credit card companies especially. Call the number on the back of your card, tell them you’re struggling and want to stay current but need a lower interest rate. Ask to be put on a hardship program. If you’ve been a customer for a few years and mostly paid on time, they often say yes. The worst they can do is say no.

Also look into nonprofit credit counseling — it’s free. Nonprofit credit counseling agencies (look for NFCC-affiliated organizations) can negotiate with your creditors on your behalf to lower interest rates and consolidate payments into one. This is called a Debt Management Plan (DMP). You pay the agency one amount per month; they distribute it. Fees are very low or waived if you qualify. This is not the same as debt settlement (which trashes your credit) or predatory debt consolidation loans.

How Do I Make a Budget When There’s Nothing Left at the End of the Month?

Use a zero-based budget — not to find savings, but to stop leaks. A zero-based budget means you assign every dollar a job on paper before the month starts. You’re not trying to find money to save. You’re trying to stop the slow leak of small unplanned purchases that, at the end of the month, you can’t account for. $14 here. $23 there. Over a month, that’s often $80 to $150 that disappeared without anything to show for it. Apps like EveryDollar (free version) or even a notebook work. The point is that every dollar has a name before you spend it.

Can I Get Help With Debt If My Credit Is Already Wrecked?

Yes, and your credit score matters less than you think at this stage.

Check if you qualify for government or community assistance. If you’re earning under $40k, you may qualify for programs you don’t know about. LIHEAP helps with energy bills. Medicaid can cover medical debt you’re drowning in. 211.org (call or text 211) connects you to local assistance for food, utilities, and housing costs — freeing up cash for debt. Your state may also have emergency rental assistance or utility programs still running.

Understand when bankruptcy might actually make sense. Bankruptcy isn’t failure — it’s a legal tool. Chapter 7 bankruptcy can wipe out most unsecured debt (credit cards, medical bills, payday loans) within 3 to 6 months. If your income is low enough, you may qualify. It does serious damage to your credit for 7 to 10 years, but if your credit is already destroyed and the debt is unpayable, it may be the reset you need. Speak with a bankruptcy attorney — many offer free consultations, and legal aid societies provide free advice to low-income workers.

What If My Income Just Isn’t Enough No Matter What I Do?

Then debt management alone isn’t the full answer. You need more income — even temporarily.

Ask your current employer about overtime, even one shift a week. Sell things you own and don’t use — Facebook Marketplace and OfferUp take minutes to list. Offer local services (moving help, lawn care, driving people) through apps or word of mouth. If your job has on-call or weekend shifts that pay more, take them for a defined period — say three months — with a specific debt target in mind. The goal isn’t to work yourself into the ground forever. It’s to generate a short burst of extra money to pay off one high-interest debt and break the cycle.

Another option is to simply change careers, if you have no degree we’ve written a blog just for that here.

One Honest Truth About Debt and Low-Income Work in 2026

The economy is hard right now in ways that aren’t your fault. Job listings are up but real wages haven’t kept up with costs. Remote work opportunities that pay better often require credentials most physical workers don’t have time or money to get. The financial advice industry does not speak to you — it’s built for people with savings to optimize.

The steps above won’t solve everything overnight. What they will do is stop the situation from getting worse, reduce the amount you’re bleeding to interest, and give you a path forward that doesn’t require a miracle. You deserve advice that treats you like an intelligent adult dealing with genuinely hard circumstances — because that’s exactly what you are.

Work with HTF

Need a real plan with step-by-step guidance?

If you’re trying to change careers, fix your money, or both at the same time, you probably don’t need another lecture about discipline. You need someone to help you look at the actual numbers, the actual job options, and the next step that won’t make your life harder.

That’s what Hit The Fan coaching is for. Work with Greg on the 6-Month Stability Plan, one-on-one coaching, or a realistic no-degree career path that fits your actual life.

No lectures. Just the next better step.

Frequently Asked Questions

The most effective approach on a low income is to list all debts with their interest rates, pay minimums on everything to stay current, then direct any additional funds — even small amounts — toward the highest-interest debt first. Simultaneously, contact creditors directly to request hardship programs or reduced interest rates, and seek help from nonprofit credit counseling agencies that can negotiate on your behalf for free.

Getting out of debt while living paycheck to paycheck requires three things: stopping new debt from accumulating, reducing what you’re paying in interest through hardship programs or nonprofit DMPs, and finding even small amounts of additional income on a temporary basis. Government assistance programs for utilities, food, and healthcare can free up dollars that then go toward debt repayment.

A debt management plan (DMP) is an arrangement where a nonprofit credit counseling agency negotiates lower interest rates with your creditors and consolidates your payments into one monthly amount. It typically takes three to five years to complete and does not require good credit to start. For people struggling with multiple credit card or unsecured debts, it is often one of the most effective and least harmful options available.

Mathematically, paying off the highest interest rate first saves more money. Psychologically, paying off the smallest balance first provides faster motivation and many people stick to it better. Both strategies work — the best one is whichever you will actually follow through with. The avalanche method is ideal if you have payday loans. The snowball method is often better for people who need a quick win to stay committed.

Yes. Nonprofit credit counseling, hardship programs through existing creditors, government assistance for living costs, and bankruptcy are all available regardless of credit score. Debt management plans through NFCC-affiliated agencies do not require good credit. Legal aid societies provide free bankruptcy consultations to low-income workers. Bad credit does not eliminate your options — it just changes which options make the most sense.

Chapter 7 bankruptcy can be a legitimate solution for low-income workers when unsecured debt — credit cards, medical bills, payday loans — has reached a level that cannot realistically be repaid given current income. It discharges most unsecured debt within months but damages credit for seven to ten years. It is best considered when the debt is so large that even a structured repayment plan would take more than a decade, and when the credit damage is less harmful than continuing to carry the debt.

Low-income workers may qualify for LIHEAP energy assistance, Medicaid or CHIP for medical costs, SNAP for food, emergency rental assistance programs administered through local governments, and 211 community services that connect people to local nonprofit resources. These programs reduce living expenses, freeing income that can go toward debt repayment instead.